Vasicek (1977) assumed that the instantaneous spot rate under the real-world measure evolves as an Ornstein-Uhlenbeck process with constant coefficients. The Vasicek model is one of the earliest no-arbitrage interest rate models based upon the idea of mean reverting interest rates, and that gives an explicit expression for the (zero-coupon) yield curve.

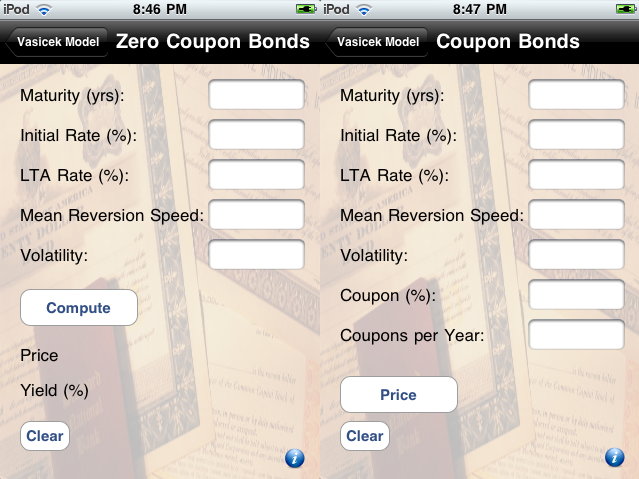

Zero-Coupon Bonds

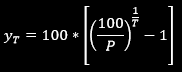

The price of a pure-discount (zero-coupon) bond under the model can be derived by the following expression:

Zero-Coupon Bonds

The price of a pure-discount (zero-coupon) bond under the model can be derived by the following expression:

The model takes 5 parameters as inputs:

· T = Bond Maturity in years

· r(0) = Initial interest rate at time 0 in percent

· k = Speed of Mean Reversion

· θ = Long Term Average rate in percent

· σ = Volatility

The model computes the price, P(0,T) from the above expression, of the zero coupon bond and derives the respective (zero coupon) yield. The yield is derive assuming a face value of 100 and annual compounding, using the following expression:

· T = Bond Maturity in years

· r(0) = Initial interest rate at time 0 in percent

· k = Speed of Mean Reversion

· θ = Long Term Average rate in percent

· σ = Volatility

The model computes the price, P(0,T) from the above expression, of the zero coupon bond and derives the respective (zero coupon) yield. The yield is derive assuming a face value of 100 and annual compounding, using the following expression:

where P is the zero coupon price, T is its maturity in years, and yT is its corresponding zero coupon yield in percent.

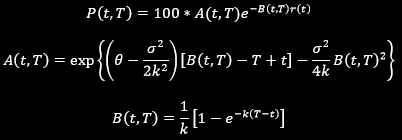

Coupon Bonds

In the case of coupon bonds pricing, the model takes two additional parameters as inputs:

· c = coupon payment as a percent of face value (assumed 100)

· m = number of coupon payments per year

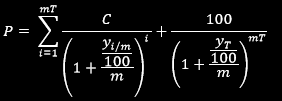

The coupon bond is priced using the following expression:

Coupon Bonds

In the case of coupon bonds pricing, the model takes two additional parameters as inputs:

· c = coupon payment as a percent of face value (assumed 100)

· m = number of coupon payments per year

The coupon bond is priced using the following expression:

where:

· C is the value of the coupon at each coupon payment: C = (c/100) / m

· yi is the yield given by the zero-coupon yield curve (in above section) at time ‘i’

· C is the value of the coupon at each coupon payment: C = (c/100) / m

· yi is the yield given by the zero-coupon yield curve (in above section) at time ‘i’