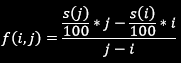

Given the ‘i’ year spot rate s(i) and ‘j’ year spot rate s(j) (where: j > i) in percent, the implied (j – i) year forward rate f(i,j), ‘i’ years from now is the rate of interest between those times that is consistent with a given spot rate curve. . Assuming an ‘m’ period-per-year compounding convention, we compute the forward rate as

follows:

follows:

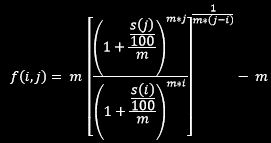

For continuous compounding, the forward rate is computed as follows:

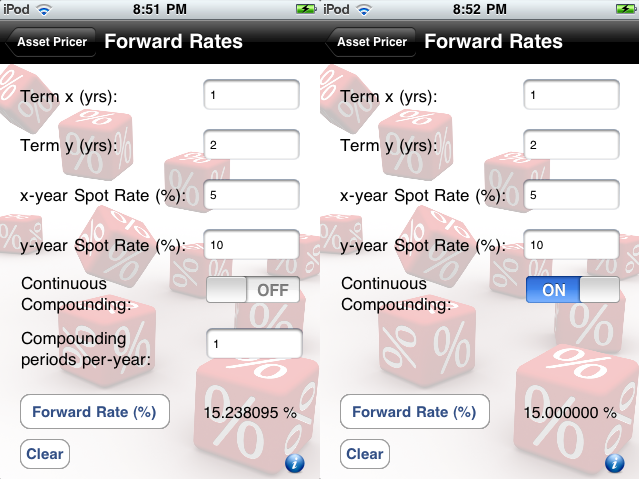

The user is asked to input the ‘x’ year and ‘y’ year spot rates in percent along with their respective ‘x’ and ‘y’ terms in years. The user is also asked to determine the compounding convention (continuous vs discrete). This is done by prompting the user to “switch” continuous compounding ON or OFF. Notice how switching continuous compounding OFF hides the “Compounding periods per-year” label and text box, associated with discrete compounding. The switch is set to OFF by default (as the module is first accessed).