Consider a portfolio of N stocks, with stock i’s return having mean E(ri) and variance var(ri) =σi2. Covariance of stock i with stock j is given by cov(ri,rj) = ρij σi σj.

The return of the portfolio is:

The return of the portfolio is:

Where wi = ($ value of stock i’s position)/(total $ value of portfolio).

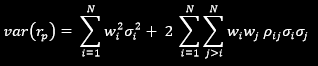

The variance of the return on this portfolio is:

The variance of the return on this portfolio is:

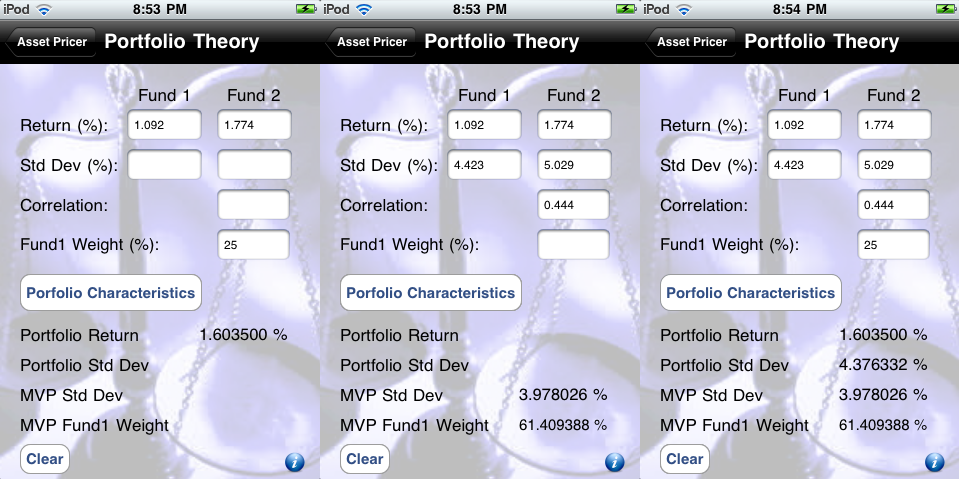

Two-Fund Portfolio

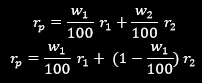

Consider a portfolio consisting of two assets (N = 2) of correlation ρ (where -1<ρ<1), with weights of w1 and w2, means μ1 and μ2, and volatilities σ1 and σ2. Assume all parameters are input by the user in percent. The portfolio’s return (in percent) in this case would be:

Consider a portfolio consisting of two assets (N = 2) of correlation ρ (where -1<ρ<1), with weights of w1 and w2, means μ1 and μ2, and volatilities σ1 and σ2. Assume all parameters are input by the user in percent. The portfolio’s return (in percent) in this case would be:

The portfolio’s variance would be:

The Portfolio’s standard deviation (in percent) would be:

The Minimum Variance Portfolio (MVP) has the following variance:

The Minimum Variance Portfolio would thus have a standard deviation (in percent) of:

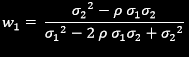

To form the Minimum Variance Portfolio, w1 (contribution of asset 1 to value of portfolio) should be: